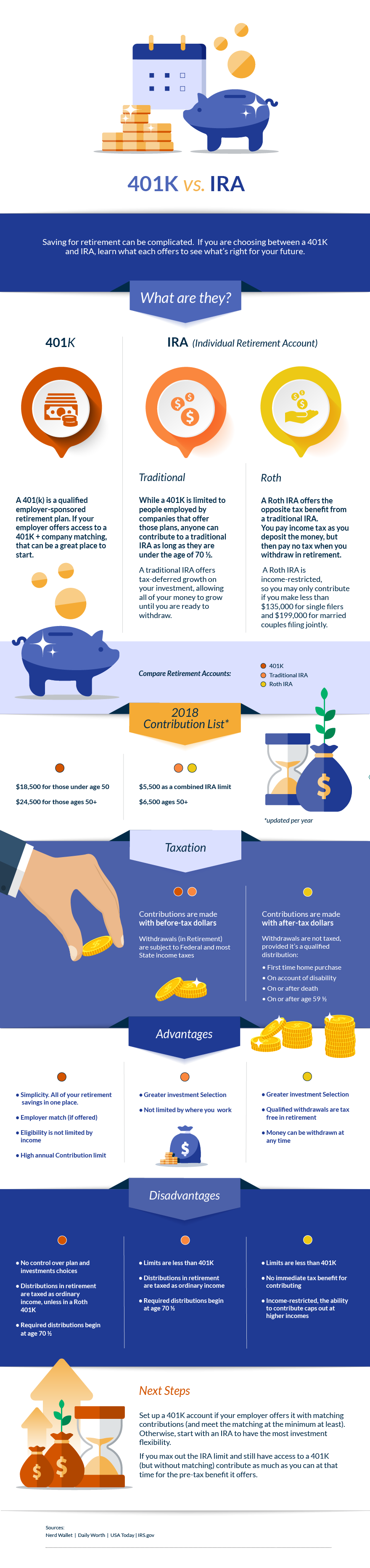

Saving for retirement can be complicated. If you are choosing between a 401K and IRA, learn what each offers to see what’s right for your future.

|

401K |

IRA (Individual Retirement Account) |

|

|

|

Traditional |

Roth |

|

What are they? |

||

|

A 401(k) is a qualified employer-sponsored retirement plan. If your employer offers access to a 401K + company matching, that can be a great place to start. |

While a 401K is limited to people employed by companies that offer those plans, anyone can contribute to a traditional IRA as long as they are under the age of 70 ½. A traditional IRA offers tax-deferred growth on your investment, allowing all of your money to grow until you are ready to withdraw. |

A Roth IRA offers the opposite tax benefit from a traditional IRA. You pay income tax as you deposit the money, but then pay no tax when you withdraw in retirement.

A Roth IRA is income-restricted, so you may only contribute if you make less than $135,000 for single filers and $199,000 for married couples filing jointly. |

|

2018 Contribution Limit* updated per year |

||

|

$18,500 for those under age 50; $24,500 for those ages 50+ |

$5,500 as a combined IRA limit; $6,500 ages 50+ |

|

|

Taxation |

||

|

Contributions are made with before-tax dollars

Withdrawals (in Retirement) are subject to Federal and most State income taxes |

|

Contributions are made with after-tax dollars

Withdrawals are not taxed, provided it’s a qualified distribution:

|

|

Advantages |

||

|

|

|

|

Disadvantages |

||

|

|

|

|

Next Steps |

||

|

Set up a 401K account if your employer offers it with matching contributions (and meet the matching at the minimum at least). Otherwise, start with an IRA to have the most investment flexibility. If you max out the IRA limit and still have access to a 401K (but without matching) contribute as much as you can at that time for the pre-tax benefit it offers. |

||

|

Sources: Nerd Wallet | Daily Worth | USA Today | IRS.gov |

||